Optimizing Bank Performance through Loan Recovery in Nigeria: A Comprehensive Analysis of Loan Recovery Strategies of Ecobank Plc.

Akaninyene Billy Orok*  , Effiong Asuquo Okon and Idongest Tim Titus

, Effiong Asuquo Okon and Idongest Tim Titus

1Department of Banking and Finance, Faculty of Management Sciences, University of Calabar, Calabar Nigeria .

http://dx.doi.org/10.12944/JBSFM.05.01.04

Copy the following to cite this article:

Orok A. B, Okon E. A, Titus I. T. "Optimizing Bank Performance through Loan Recovery in Nigeria: A Comprehensive Analysis of Loan Recovery Strategies of Ecobank Plc".Journal of Business Strategy Finance and Management, 5(1).

DOI:http://dx.doi.org/10.12944/JBSFM.05.01.04

Copy the following to cite this URL:

Orok A. B, Okon E. A, Titus I. T. "Optimizing Bank Performance through Loan Recovery in Nigeria: A Comprehensive Analysis of Loan Recovery Strategies of Ecobank Plc".Journal of Business Strategy Finance and Management, 5(1). Available here:https://bit.ly/44W9JNf

Download article (pdf) Citation Manager Publish History

Introduction

Banks faces challenges when it comes to debt recovery from customers. Most bank customers are inaccessible after loan has been granted to them, and this makes it difficult for banks to recover loan lend to their customers (Ghandi, 2014). Debt recovery simply means following loans that has not been paid by a borrower with the intention of getting the delinquent obligations paid back. Banks faced challenges due to default in payment by borrowers, and lack of credit management of debt portfolio which leads to a slack in the quality of bank statement.

According to Cambridge School of Finance (2016), debt recovery is the process of getting people or businesses to pay back money they owe to other people or businesses at a time that was set by two parties. Meghana & Supriya (2020) opines that the commercial banks are key players in the banking industry though financial inclusion in developed nation.

The popularity of commercial banks, according to Afolabi (1991), is not due to the realization that they represent legally or commercially middlemen in the structure, but instead due to their vast branch network, sizable client base, and simplicity of transacting with them. The commercial banks' role as intermediaries reaches its zenith when they extend credit facilities like loans and investments, making money available to individuals and businesses. Because of this one role, commercial banks contribute to the rise in social economic activity. (Frattaroli & Herpfer, 2023)

According to Frattaroli & Herofer (2023), banks must choose between specialty and diversity when deciding on their lending portfolio. A basic argument for portfolio diversification contends that banks should disperse lending risk among several businesses. And monitoring strategies is the best option a bank can formulate to make sure that the loan granted to a borrower is used for the exact purpose (Migwi, 2013; Cerqueiro, Ongena, & Roszbach, 2016; Bhat & Desai, 2020), focus on the strategies adopted by commercial banks to monitor loan given to a customer.

Each bank has its own method for recovering debt from customers in order to improve performance, guarantee that loans given to customers are repaid, and guarantee that the bank will continue to function normally. According to Greuning and Igbal (2007), banks can prevent loan losses before they occur.

According to Muiru, Oluoch and Ajang (2018), the likelihood that loans will be paid back in full, including interest and principal, is another factor that influences the loan portfolio's value. The majority of commercial banks' primary business is lending. Typically, the loan portfolio is the largest asset and primary revenue source. As a result, it is one of the greatest threats to a bank's stability. Loan portfolio issues have historically been the primary cause of bank losses and failures, whether as a result of lax credit standards, inadequate portfolio risk management, or economic weakness.

Recovery process by a bank is to speed up payment from their customers. Granting of credit to customers is one of the ways banks generate funds for payment of salaries, taxes, dividend, and also retain earnings, but it becomes difficult because most customers default in payment, and this affect the bank statement, and growth of the bank. This makes banks to come up with procedures to recover loan granted to a customer.

Objective of the study

The objective of this study is to understand the several means banking sector in Nigeria recover loans, and how they monitor such loans, but specifically,

- To determine the influence of debt outstanding on bank performance.

- To establish the effect of recovered funds on bank performance.

- To assess the relationship between loan customer retention and bank performance

- To investigate how loan customer relationship impacts bank performance

In the process of our investigation, we will proffer answers to the following questions.

- Does the level of debt outstanding affect the profitability of banks?

- How does the recovery of funds from non-performing assets contribute to the health of banks?

- How does loan customer retention relate to the overall profitability and revenue generation of banks?

- What is the role of strong customer relationships in enhancing the performance of banks?

Research hypotheses

The following hypothesis is proposed for test in the study

- There's no significant relationship between outstanding debt, and banks profitability.

- There's no significant relationship between recovered funds, and profitability.

- loan customer retention has no influence on the bank profitability

- loan customer relationship does not impacts bank performance

Theoretical framework

Several theories have been propounded that supports credit recovery. Notably among them include Credit Theory of Money and Customer-Supplier Relationship Theory.

The British economist Mitchell Innes also contributed to the development and popularization of the credit theory of money in his 1913 paper "What is Money?" According to the credit theory of money, which is a form of credit produced by financial organizations via the extension of financial assistance and other types of credit, money does not constitute a tangible good. Rather, it is a form of credit. According to this idea, money is produced as a result of these institutions' borrowing and lending operations and is not backed by any tangible goods like gold or silver. The theory goes on to claim that the demand for money determines its value, while the supply of money is governed by the total amount of credit produced by these organizations. According to Innes (1914), to that a sale and purchase is the exchange of a commodity for credit. From this main theory springs the sub-theory that the value of credit or money does not depend on the value of any metal or metals, but on the right which the creditor acquires to "payment," that is to say, to satisfaction for the credit, and on the obligation of the debtor to "pay" his debt and conversely on the right of the debtor to release himself from his debt by the tender of an equivalent debt owed by the creditor, and the obligation of the creditor to accept this tender in satisfaction of his credit.

In Hamisu (2017), Robert and Gary's Customer-Supplier Relationship Theory is discussed. Customer-supplier relationship theory suggests that debt recovery techniques have costs and benefits for both lenders and borrowers. As part of a debtor-creditor relationship, there are four types of costs: pre-sale, post-sale, distribution, and production costs.

Among the primary benefits, Brealey and Meyers (2005) cite customer economics, power, the nature of the decision-making unit, and the institutional connection between creditor and debtor. Because of this, the debtor and the creditor will always enjoy wide profit margins, depending on the interest rate on the loan. In order to manage separate client-supplier associations, the protectors of this speculation use a portfolio method. In this theory, debt recovery strategies play a significant role in financial institutions' performance since the repayment of debt is a matter of association between a creditor and a debtor in order to maintain mutual interests in terms of gains for both parties(Kaczmarczyk, 2019).

Empirical reviews

In their respective studies, Salas and Saurina (2002), Ali and Daly (2010), and Nkusu (2011) discovered that non-performing loans and GDP per capita had an inverse relationship. On the other hand, Beck, Demirhuc-Kunt, and Levine (2013) discovered that non-performing loans and GDP had an appositive relationship.

Araka (2018) investigated the impact of non-performing loans (NPLs) on the financial performance of commercial banks in Nigeria. In order to evaluate data from the Central Bank of Nigeria's (CBN) statistical bulletin and publications from the Nigeria Deposit Insurance Corporation (NDIC), the research used a variety of regression approaches. The data showed that a high ratio of non-performing loans to total loans and a high cash reserve ratio had a statistically significant negative influence on return on assets (ROA). This shows that a high percentage of non-performing loans may have a negative impact on the financial health of Nigeria's commercial banks.

Again, multiple regression modeling was used in an investigation on loans with poor performance by Gabriel, Victor, and Innocent (2019) to look at data gathered from the Central Bank of Nigeria (CBN) statistical bulletin and Nigeria Deposit Insurance Corporation (NDIC) publications over a range of years. The ratio of non-performing loans to total loans (NPL/TLR) and the cash reserve ratio (CRR) both have statistically significant negative effects on return on assets (ROA). These findings suggest that a high proportion of non-performing loans may have a negative impact on the financial health of Nigerian commercial banks. Therefore, it is advised that regulatory bodies in Nigeria maintain an atmosphere that encourages and supports effective risk management techniques among the nation's commercial banks.

Bos and Kolari (2005) state that banks with a relatively low equity-asset ratio are likely to experience excessive losses. According to Salas and Saurina (2002) and Berger and DeYoung (2007), there is a negative correlation between the capital ratio and nonperforming loans.

Using financial ratios gathered from the financial books of the selected banks and analyzed using regression, correlation, and descriptive statistical techniques, Kargi (2011) examined the effect of credit risk on the profitability of Nigerian banks. According to his findings, credit risk management has a significant impact on bank profitability in Nigeria. The study came to the conclusion that bank profitability was inversely correlated with the amount of loans and advances, deposits, and non-performing loans, putting banks at risk of distress and illiquidity.

According to a similar study by Epure and Lafuente (2012), regulatory changes improve bank performance, while the ratio of capital adequacy to net interest margin has a positive effect while risk revealed NPLs and differences in banks have a negative impact on the return on asset. Kithinji (2010) who analyzed the effect of credit risk the board on business banks benefit in Kenya showed that, NPLs and measure of credit doesn't impact the degree of business bank productivity, thusly the suggested that factors other than NPLs and credit in all actuality do influence benefits.

From 2005 to 2008, credit risk efficiency in Taiwanese commercial banks was examined by Chen and Pan (2012). Using data envelopment analysis (DEA), they looked at credit risk through the lens of financial ratios. Credit risk cost efficiency (CR-CE), credit risk allocative efficiency (CR-AE), and credit risk technical efficiency (CR-TE) were the proxies for credit risk. Over the time periods analyzed, their findings revealed that banks could be efficient in all efficiency categories. In general, the DEA analysis revealed that CR-CE, CR-AE, and CR-TE had relatively low average efficiency levels in 2008. The results of Felix and Claudine's (2008) study on the relationship between credit risk management and bank performance revealed that ROA and ROE were inversely related to the NPLs ratio to total loans, resulting in a decline in performance.

According to Ahmad and Ariff (2007)'s investigation, regulation is very important for banks that specialize in multiple products and services; whereas a bank's management quality is crucial for a loan-dominated institution in an emerging market. They assert that a significant contributor to the facilitation of potential credit risk is an increase in the provision for loan losses. They came to the conclusion that developed markets have lower credit risk than emerging markets.

The investigation of Al-Khouri (2011) on the impact of the attributes of bank's particular gamble and the working climate on banks execution in the Bay Collaboration Committee (GCC) utilized the proper impact relapse methods and presumed that, capital gamble, liquidity chance and credit risk are the dominants components that influences the exhibition of banks while estimated utilizing ROA, and just liquidity risk significantly affects the presentation of the banks with regards to ROE.

According to Ahmed, Takeda, and Shawn (1998), an increase in the provision for loan losses reflects an increased deterioration in credit risk and loan quality, thereby affecting banks' performance. The procedures for overseeing credit risk are the systems applied by banks to get away or diminish the adverse consequence of credit risk. It is essential for banks to have a solid framework for managing credit risk if they are to achieve their goals and remain in business.

From the aforegoing, reviews revealed a predominant research focus on either non-performing loans or Credit Risk Management Practices and Internal Control Systems, as well as their associations with financial performance. Existing literature primarily relied on secondary data obtained from the Central Bank and National Deposit Insurance Corporation to assess the influence of credit recovery. The outcomes of these studies varied depending on the utilization of multiple regression analysis to examine the relationships between dependent and independent variables (Salas & Saurina, 2002; Ali & Daly, 2010; Nkusu, 2011; Omitogun, Olanrewaju, & Alalade, 2016; Araka, 2018; Gabriel, Victor&Innocent, 2019; Abimbola, 2020). Studies that deviated from these, are in developed economies and not a developing economy.

In contrast, the present study departs from relying solely on secondary data and instead delves into the exploration of field data. This approach involves gathering insights from interviews and questionnaires, allowing respondents to provide experiential perspectives on various credit recovery-related matters. By adopting this methodology, a more comprehensive understanding of the subject matter can be obtained, thereby enriching the analysis and contributing to the existing body of knowledge in the field of finance

Research Design

A research design refers to an overall plan of combining different components of the research study in an organized manner. This study uses a descriptive design to better explain the connection between loan repayment, credit, and debt recovery. A survey research design was employed in selecting a few individuals from a group in other to gather relevant information concerning the subject matter. The research is based on qualitative, and quantitative techniques in collecting relevant data through a questionnaire.

Population of the Study

A population is made up of all conceivable elements or observations relating to a particular phenomenon of interest of the research subject or element. The population of this study comprised of credit department staff of branches of Ecobank Nigeria Plc in Cross River State, who are in charge of structuring, availing and recovery of credits at the branch level.

Ecobank Plc

Ecobank Nigeria is a significant subsidiary of Ecobank Transnational Incorporated (ETI), One of the Africa’s leading independent banking group which was established as a public limited liability company on October 7, 1986. Using digital platforms like the Ecobank Mobile App, USSD, Ecobank Online, Ecobank OmniPlus, Ecobank Omnilite, EcobankPay, and Ecobank RapidTransfer, as well as an extensive distribution network of over 250 branches and over 50,000 agency banking locations, Ecobank is a major player in the distribution of financial services in Nigeria.

Ecobank Nigeria is now a top-tier Nigerian bank in terms of assets, customer base, deposits, and branches thanks to the Ecobank group’s successful acquisition of Oceanic Bank International. Ecobank had previously acquired the defunct All States Trust Bank Plc, Hallmark Bank Plc, and African International Bank Plc (AIB) customers and deposit liabilities.

The population of the study covers marketing officers in branches of Cross River State who have credit portfolios to drive recovery.

Table 1: Population of the Study

|

S/N |

Branch |

No of Staffs |

|

|

1 |

Mary Slessor Road Branch, Calabar

|

Consumer Banking Group |

6 |

|

Commercial Banking Group |

3 |

||

|

Corp/Investment Banking Group |

4 |

||

|

2 |

M/M Highway Branch, Calabar |

Consumer Banking Group |

3 |

|

Commercial Banking Group |

2 |

||

|

Corp/Investment Banking Group |

2 |

||

|

3 |

Etta Agbor Road Branch, Calabar |

Consumer Banking Group |

3 |

|

Commercial Banking Group |

2 |

||

|

Corp/Investment Banking Group |

2 |

||

|

4 |

Hospital Road Branch, Ogoja |

Consumer Banking Group |

3 |

|

Commercial Banking Group |

2 |

||

|

Corp/Investment Banking Group |

2 |

||

|

5 |

Calabar Road Branch, Ikom |

Consumer Banking Group |

2 |

|

Commercial Banking Group |

2 |

||

|

Corp/Investment Banking Group |

2 |

||

|

Total no of Credit Staff |

40 |

||

Sample Size

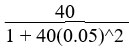

The Taro Yamane formula was used to determine the sample size due to the large

number of the population.

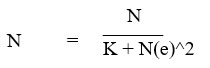

N = Population of study

K = Constant(1)

e = degree of error expected

n=sample size

Validity and Reliability of Instrument.

To ensure the validity of the research instrument, the researcher submitted the research questionnaires to the supervisor for scrutiny and approval. In order to determine the reliability of the research instrument, the researcher gave out 5 copies of the questionnaire to respondents outside the study area; this was to test ability of the respondents to understand the questions asked in the questionnaire. This was used to standardize the questionnaire. Through this process, the questionnaire was proven to be reliable

Method of Data Analysis

Data for the study were analyzed using frequency distribution table, and percentages will be used to analyze the data from the questionnaire, with and correlation with the use of SPSS were used to tests the hypotheses.

P = No. of responses (×) × 100

Total numbers of responses(y)

Also considered a chi-squared test is a test in which this is asymptoticallytrue, meaning that the sampling distribution (if the null hypothesis is true) can be made to approximate a chi-squared distribution as closely as desired by making the sample size large enough.

Formula:

For the Chi Square distribution of

is the Gamma function:

X²= Σ (observed frequencies-expected frequencies)²

Expected frequency

e x²= Σ (E-O) ²

Where as:

X² = chi-square

Σ = summation or sigma

Fo = observed distribution

Fe = Expected distribution

Expected value:

Σ rc = Row total x column total

We used expected counts for three variables - Customer Relationship, Quality of Service, and Loan Customer Retention - to conduct Chi-square tests. Chi-square tests are a type of statistical test used to determine if there is a significant association between two categorical variables. The expected counts refer to the number of observations that would be expected in each category if there was no association between the variables.

By comparing the expected counts to the actual counts, the researchers were able to determine if there was a significant association between the variables. Only the expected counts for the three variables were subjected to the Chi-square test, indicating that these variables were the main focus of the research questions.

The statistical analysis is presented as Chi-square test statistics and exact significance (p-values), which are used to determine the probability of obtaining the observed results by chance. All tests were conducted at a significance level of P = .05, which means that the researchers considered a p-value less than .05 to be statistically significant. Accordingly, one-sample t-tests was adopted for comparisons between groups and it was used because they are considered more powerful than other types of t-tests in certain situations.

Table 2: Variables

|

Dependent Variable |

Definitions |

|

Bank Performance Evaluation of a bank's overall financial and operational health, efficiency, and effectiveness in achieving its objectives

|

|

|

Independent Variable |

Definitions

|

|

Loan Customer Retention Customers Retention involves understanding the elements affecting borrowers' decisions to continue their loans with the same institution for a long time.

|

|

|

Customer Relationship

|

|

|

Recovered Funds Assets that have been successfully collected or reclaimed after a period of delinquency or non-payment. |

|

|

Outstanding Debt Obligations Total amount of money that an individual, business, or entity owes to banks and it has not yet been fully repaid or settled. |

|

Data Presentation And Analysis

Section A

|

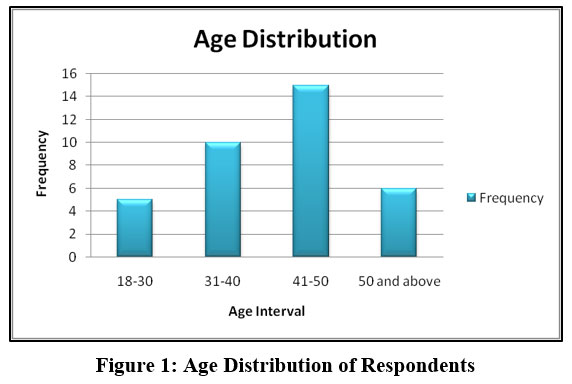

Figure 1: Age Distribution of Respondents Click here to view Figure |

Table 3: Age distribution of Respondents

|

Age Interval |

Frequency |

Percentage % |

|

18-30 |

5 |

13.9 |

|

31-40 |

10 |

27.9 |

|

41-50 |

15 |

41.7 |

|

50 and above |

6 |

16.7 |

|

Total |

36 |

100 |

Source: Field Survey, 2023

Table 3: shows that 41.7% of the total respondents are within the age range 41-50, 27.9% are within the age 31-40, 13.9% are within the age 18-30 and 16.7% are within the age range of 50 and above made a percentage of 100.

|

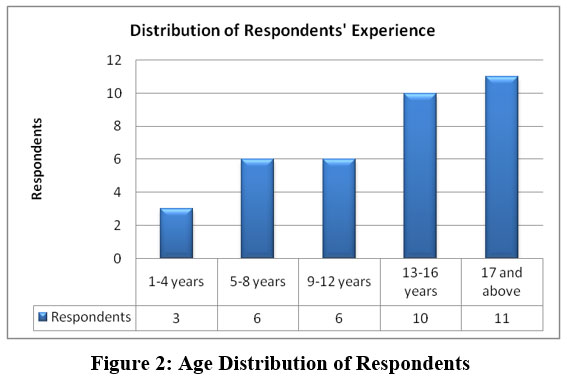

Figure 2: Age Distribution of Respondents Click here to view Figure |

Table 4: Experience distribution of Respondents.

|

Experience |

Respondents |

Percentage% |

|

1-4 years |

3 |

5 |

|

5-8 years |

6 |

15.5 |

|

9-12 years |

6 |

21.1 |

|

13-16 years |

10 |

20.4 |

|

Total |

11 |

38.1 |

Table 4:Shows that 5% of the respondent have an experience of 1-4 years, 15.5% are 5-8 years’ experience, 21.1% are 9-12 years’ experience, 20.4% are 13-16 years and 38.1% for 17 years and above.

|

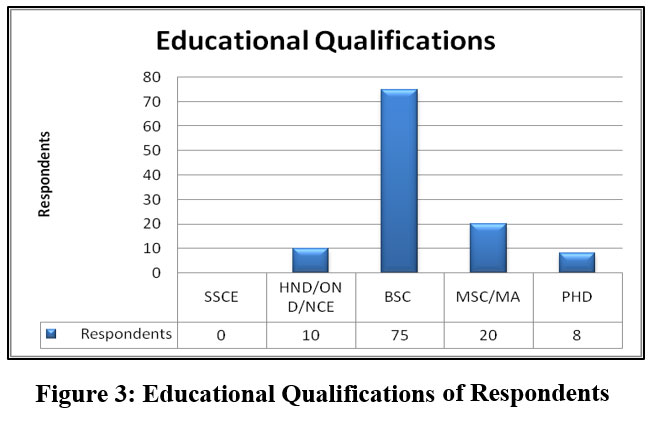

Figure 3: Educational Qualifications of Respondents Click here to view Figure |

.

Table 5: Educational qualification of Respondents

|

Educational Qualification |

Respondents |

Percentage% |

|

SSCE |

0 |

0 |

|

HND/OND/NCE |

10 |

8.8 |

|

BSC |

75 |

66.4 |

|

MSC/MA |

20 |

17.7 |

|

Ph.D |

8 |

7.1 |

|

Total |

113 |

100.0 |

Source: Field Survey, 2023

Table 5:Shows that 8.8% of respondent are HND/OND/NCE holders, 66.4% are BSC degree holders, 17.7% are MSC/MA holders and 7.1% are PHD holders

|

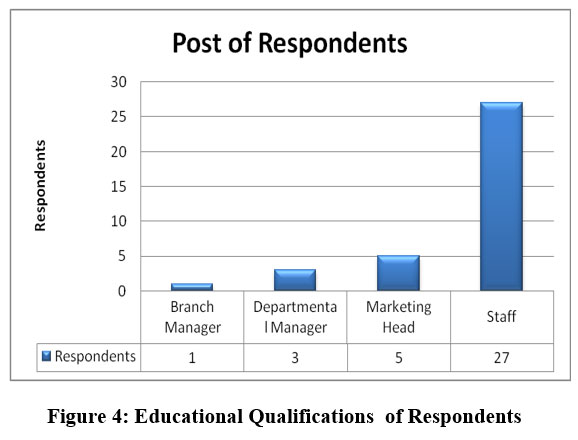

Figure 4: Educational Qualifications of Respondents Click here to view Figure |

Table 6: Post of Respondents

|

Post |

Respondents |

Percentage% |

|

Branch Manager |

1 |

2.7 |

|

Departmental Manager |

3 |

6.2 |

|

Marketing Head |

5 |

20.4 |

|

Staff |

27 |

70.8 |

|

Total |

36 |

100.0 |

Table 6:shows that 2.7% of the total respondents are branch manager, 6.2% are Departmental Manager, 20.4% Marketing Head and 70.8% are just staffs.

Test of hypothesis

The stated hypothesis are tested using the Chi-square statistics at 5% level of significance.

The degree of freedom (DF) is given as:

R-D (C-1)

Where R = number of rows

C = number of columns

Decision rule

the decision rule state that reject the null hypothesis (Ho) when the calculated X2 value is greater than the critical X2 value. Otherwise accept the null hypotheses (Ho) and reject the alternate hypothesis (Ho) when the calculated X2 value is lesser than the critical X2 value.

Hypothesis One

There is no significant relationship betweencustomer service relationships and bank profitability.

Table 7: Cross tabulation of the relationship between Customer relationship and Bank profitability

|

|

Bank Profitability |

Total |

|||||

|

Strongly Agreed |

Agreed |

Disagreed |

Strongly Disagreed |

||||

|

Customer Relationship |

Strongly Agreed |

Count |

3 |

19 |

1 |

0 |

23 |

|

Expected Count |

4.5 |

12.4 |

4.1 |

2.0 |

23.0 |

||

|

Residual |

-1.5 |

6.6 |

-3.1 |

-2.0 |

|

||

|

Agreed |

Count |

8 |

35 |

11 |

8 |

62 |

|

|

Expected Count |

12.1 |

33.5 |

11.0 |

5.5 |

62.0 |

||

|

Residual |

-4.1 |

1.5 |

.0 |

2.5 |

|

||

|

Disagreed |

Count |

1 |

2 |

5 |

2 |

10 |

|

|

Expected Count |

1.9 |

5.4 |

1.8 |

.9 |

10.0 |

||

|

Residual |

-.9 |

-3.4 |

3.2 |

1.1 |

|

||

|

Strongly Disagreed |

Count |

10 |

5 |

3 |

0 |

18 |

|

|

Expected Count |

3.5 |

9.7 |

3.2 |

1.6 |

18.0 |

||

|

Residual |

6.5 |

-4.7 |

-.2 |

-1.6 |

|

||

|

Total |

Count |

22 |

61 |

20 |

10 |

113 |

|

|

Expected Count |

22.0 |

61.0 |

20.0 |

10.0 |

113.0 |

||

Chi-square Test

|

Pearson Chi-square |

42.970 |

|

Degree of Freedom |

9 |

|

P-value |

0.0905 |

Source: field survey 2023.

Level of significance =0.05

The result as shown above in table indicates that that the Calculated X2 value of 42.970 is greater than the Critical X2 value of 0.0905 at 0.05 level of significance with a 9 degree of freedom. The null hypothesis is rejected while the alternate hypothesis accepted. Thus; there is a significant relationship between customer service relationships and bank profitability.

Hypthoesis Two

Decision rule: the decision rule state that reject the null hypothesis (Ho) when the calculated X2 value is greater than the critical X2 value. Otherwise accept the null hypotheses (Ho) and reject the alternate hypothesis (Ho) when the calculated X2 value is lesser than the critical X2 value.

There is no significant relationship between recovered funds and bank profitability.

Table 8: Cross tabulation of the relationship between recovered funds and Bank profitability

|

|

Bank Profitability |

Total |

|||||

|

Strongly Agreed |

Agreed |

Disagreed |

Strongly Disagreed |

||||

|

recovered funds |

Strongly Agreed |

Count |

8 |

36 |

6 |

6 |

56 |

|

Expected Count |

13.4 |

30.2 |

5.9 |

6.4 |

56.0 |

||

|

Residual |

-5.4 |

5.8 |

.1 |

-.4 |

|

||

|

Agreed |

Count |

5 |

13 |

2 |

7 |

27 |

|

|

Expected Count |

6.5 |

14.6 |

2.9 |

3.1 |

27.0 |

||

|

Residual |

-1.5 |

-1.6 |

-.9 |

3.9 |

|

||

|

Disagreed |

Count |

5 |

12 |

4 |

0 |

21 |

|

|

Expected Count |

5.0 |

11.3 |

2.2 |

2.4 |

21.0 |

||

|

Residual |

.0 |

.7 |

1.8 |

-2.4 |

|

||

|

Strongly Disagreed |

Count |

9 |

0 |

0 |

0 |

9 |

|

|

Expected Count |

2.2 |

4.9 |

1.0 |

1.0 |

9.0 |

||

|

Residual |

6.8 |

-4.9 |

-1.0 |

-1.0 |

|

||

|

Total |

Count |

27 |

61 |

12 |

13 |

113 |

|

|

Expected Count |

27.0 |

61.0 |

12.0 |

13.0 |

113.0 |

||

Chi-square Test

|

Pearson Chi-square |

23.354 |

|

Degree of Freedom |

9 |

|

P-value |

0.0527 |

Source: field survey 2023.

Level of significance =0.05

The result as shown above in table indicates that that the Calculated X2 value of 23.354 is greater than the Critical X2 value of 0.0527 at 0.05 level of significance with a 9 degree of freedom. The null hypothesis is rejected while the alternate hypothesis accepted. Thus; there is a there is significant relationship between recovered funds and Bank Profitability

Hypthoesis Three

Decision rule: the decision rule state that reject the null hypothesis (Ho) when the calculated X2 value is greater than the critical X2 value. Otherwise accept the null hypotheses (Ho) and reject the alternate hypothesis (Ho) when the calculated X2 value is lesser than the critical X2 value.

Table 9: Cross tabulation of the relationship between Loan Customer Retention and Bank profitability

|

|

Bank profitability |

Total |

|||||

|

Strongly Agreed |

Agreed |

Disagreed |

Strongly Disagreed |

||||

|

Customer Retention |

Strongly Agreed |

Count |

5 |

5 |

4 |

4 |

18 |

|

Expected Count |

3.8 |

11.5 |

1.4 |

1.3 |

18.0 |

||

|

Residual |

1.2 |

-6.5 |

2.6 |

2.7 |

|

||

|

Disagreed |

Count |

10 |

9 |

5 |

0 |

24 |

|

|

Expected Count |

5.1 |

15.3 |

1.9 |

1.7 |

24.0 |

||

|

Residual |

4.9 |

-6.3 |

3.1 |

-1.7 |

|

||

|

Disagreed |

Count |

9 |

47 |

0 |

0 |

56 |

|

|

Expected Count |

11.9 |

35.7 |

4.5 |

4.0 |

56.0 |

||

|

Residual |

-2.9 |

11.3 |

-4.5 |

-4.0 |

|

||

|

Strongly Disagreed |

Count |

0 |

11 |

0 |

4 |

15 |

|

|

Expected Count |

3.2 |

9.6 |

1.2 |

1.1 |

15.0 |

||

|

Residual |

-3.2 |

1.4 |

-1.2 |

2.9 |

|

||

|

Total |

Count |

24 |

72 |

9 |

8 |

113 |

|

|

Expected Count |

24.0 |

72.0 |

9.0 |

8.0 |

113.0 |

||

Chi-square Test

|

Pearson Chi-square |

53.875 |

|

Degree of Freedom |

9 |

|

P-value |

0.022 |

Source: field survey 2023.

Level of significance =0.05

The result as shown above in table indicates that that the Calculated X2 value of 53.875 is greater than the Critical X2 value of 0.022 at 0.05 level of significance with a 9 degree of freedom. The null hypothesis is rejected while the alternate hypothesis accepted. Thus; there is a There is significant relationship between customer retention and bank profitability

Hypthoesis Four

Decision rule: the decision rule state that reject the null hypothesis (Ho) when the calculated X2 value is greater than the critical X2 value. Otherwise accept the null hypotheses (Ho) and reject the alternate hypothesis (Ho) when the calculated X2 value is lesser than the critical X2

Table 10: Cross tabulation of the relationship between debt outstanding and Bank profitability

|

|

Bank profitability |

Total |

|||||

|

Strongly Agreed |

Disagreed |

Disagreed |

Strongly Disagreed |

||||

|

debt outstanding |

Strongly Agreed |

Count |

5 |

13 |

4 |

0 |

22 |

|

Expected Count |

3.9 |

8.8 |

8.8 |

.6 |

22.0 |

||

|

Residual |

1.1 |

4.2 |

-4.8 |

-.6 |

|

||

|

Agreed |

Count |

9 |

23 |

29 |

0 |

61 |

|

|

Expected Count |

10.8 |

24.3 |

24.3 |

1.6 |

61.0 |

||

|

Residual |

-1.8 |

-1.3 |

4.7 |

-1.6 |

|

||

|

Disagreed |

Count |

5 |

6 |

6 |

3 |

20 |

|

|

Expected Count |

3.5 |

8.0 |

8.0 |

.5 |

20.0 |

||

|

Residual |

1.5 |

-2.0 |

-2.0 |

2.5 |

|

||

|

Strongly Disagreed |

Count |

1 |

3 |

6 |

0 |

10 |

|

|

Expected Count |

1.8 |

4.0 |

4.0 |

.3 |

10.0 |

||

|

Residual |

-.8 |

-1.0 |

2.0 |

-.3 |

|

||

|

Total |

Count |

20 |

45 |

45 |

3 |

113 |

|

|

Expected Count |

20.0 |

45.0 |

45.0 |

3.0 |

113.0 |

||

Chi-square Test

|

Pearson Chi-square |

23.354a |

|

Degree of Freedom |

9 |

|

P-value |

0.60 |

The result as shown above in table indicates that that the Calculated X2 value of 23.354ais greater than the Critical X2 value of 0.60at 0.05 level of significance with a 9 degree of freedom. The null hypothesis is rejected while the alternate hypothesis accepted. Thus; there is a There is significant relationship between debt outstanding and bank profitability.

Discussion of Findings

The result of this study concluded that there was statistically significant impact of outstanding debt on banks performance. The finding supports the credit theory of money where money is viewed as a form of credit that is created. Borrowers incur debts from banks, which creates money, and this money circulates as a medium of trade in the economy on the assumption that the debt will be repaid. By highlighting the significance of credit creation and debt in the formation of money and the operation of the monetary system, the considerable correlation between debt outstanding and bank profitability supports the credit theory of money. Debt outstanding is a crucial component of the money supply as well as a representation of the money due to banks. Credit risk, return on equity, interest income, and other components of bank profitability are all impacted by the amount of outstanding debt. Effective debt management is crucial to preserving consumer trust in the credit system and the economy's ability to move money around. This submissions is in line with the findings of Ali, Sabir, Sajid, & Taqi (2014) who concluded that outstanding debts of banks have significant impact on bank's performance in Pakistan.

The study established that recovered funds has significant effect on bank performance. As a result of banks' involvement in circulating money through credit creation, the Credit Theory of Money acknowledges that the formation of money through credit also results in debt creation. When banks grant credit, borrowers accrue debt that must be repaid. According to the study, recovery of money has a major impact on bank performance, which may indicate that banks are skilled at handling and collecting debt. The long-term stability of the credit cycle is ensured by effective debt management, which also strengthens the connection between credit expansion and the money supply. Once more, the process of recovering money enhances banks' capacity to extend new credit, affecting the money supply and boosting economic activity. The study refutes the finding of Siraki & Yona (2021) and Kashiv (2021) who found negative relationship with non-performing loans.

Also loan customer retention by the bank had a positive effect on the on the performances of bank. In the earlier section of the article, we said that debt outstanding is a type of credit creation that, by permitting a growth of credit, helps to increase the amount of money in the economy. The amount of money in circulation in the economy as a whole rises as a result of banks' production of credit, which expands the money supply. If customers of a bank are satisfy with the services provided by the bank, it will encourage the customer to continue banking with the bank. This will in turn encourage and increase the productivity and profitability of the bank. This is in line with the assertion of Duncan and Elliot (2004) who posited that service quality has a measureable impact on customer retention, market share and profitability. Furthermore, (Dhman, 2011; Shavazi, 2013) posited that services quality is perceived important to the both organization and customers, as it would increasingly lead to higher satisfactions and loyal to the product and services brands. And Kavita et al (2022) confirmed that Bank retention strategies influences the bank

Finally, the result from the study showed a positive relationship between customer relationship and bank profitability. This implies that if much importance is given to customer relationship management, it will significantly tell on the productivity and profitability of the company. This study is consistent with the Customer-Supplier relationship theory which advocates collaboration between bank and customers on a long term basis. By taking the time to understand clients' needs, offering them individualized services, and maintaining open lines of communication will help banks better serve their clients. Customer service relationships play a crucial role in influencing borrowers' behavior. When a bank establishes strong, positive, and trustworthy relationships with its customers, it is more likely to be seen as a reliable lender. This finding is in line with a research carried out by Saka, Elegunde, and Lawal, (2014) on effects of customer relationship on bank performance in Nigeria: an empirical approach. The finding from the study posited that customer’s relationship affects banks performance. Again, Al-Wugayan (2020) established a linkage with bank performances that supports the credit theory of money in a study of customers in Kuwait. More credits leads to more interest income that translates to increased financial performance.

Conclusion

The researcher concluded that risk on debt granting cannot be remove. Most loans granted do not get repaid, so credit officers most ensure to investigate the background of the borrower before granting loans, and ensure adequate steps are put in place to recover loans before granting loan to a borrower to avoid bad debt. The investigation also concluded that a bank's total financial success is significantly impacted by the quality of its relationships with its clients. It was discovered that a strong and supportive client connection was a major contributor to the bank's increased profitability.

Additionally, client retention aided the bank's attempts to control risk. The risk of non-performing loans and credit defaults was lower since loyal clients were more likely to sustain prompt loan repayments. The bank's asset quality and overall financial stability benefited from this better credit risk management. Organizations should do more emphasizes on customers relations to convince them with products and services not only meet their needs but go further beyond their expectations (Amoako, Bandoh, & Katah, 2012; Krishnamoorthy & Srinivasan, 2013).

Recommendation

Careful observation on leading application, and the risk involve will enable the credit officer make better decisions before granting loans. But risk is inevitable, credit officers must always expect that some loans will still turn bad debt. To avoid bad debt;

- Credit officers needs to monitor outstanding debt to avoid default in payment.

- Credit officers should frequently visit the borrower to ensure the funds are used for the purpose which the loan was granted.

- Regular observation of the borrower's financial statement avoid default in payment.

- And also enforce the rules of collecting collateral before loan is granted.

- Finally, we recommend additional study on the customer retention strategies for Credit in non-banking firms.

Acknowledgement

The management and employees of Ecobank Plc are to be thanked on behalf of the writers for supplying us with the materials and knowledge required to carry out this study and finish this essay. We also thank the University of Calabar's Banking and Finance Department.

Conflict of Interest

The authors do not have any conflict of interest.

Funding

The research, writing, and/or publishing of this paper were all done without any financial assistance from organization(s) or individual(s) outside the contribution of the authors.

References

- Abimbola, Eniafe (2020), Impact of Non Performing Loan on Bank Performance in Nigeria, A Case Study of Selected Deposit Money Banks. Journal of Business & Economic Policy, 7(4), 56-70 doi:10.30845/jbep.v7n4p7

- Afolabi, L. (1991). Monetary economics. Heinemann Education books: Lagos.

- Ahmad, Nor Hayati, and Mohamed Ariff. 2007. Multi-Country Study of Bank Credit Risk Determinants. The International Journal of Banking and Finance 5: 135–52. https://doi.org/10.32890/ijbf2008.5.1.8362

- Ahmed, A. S., Takeda, C & Thomas, S (1999) “Bank loan loss provisions: a reexamination of capital management, earnings management and signaling effects”, Journal of Accounting and Economics, 28(1), 1-25 https://doi.org/10.1016/S0165-4101(99)00017-8

- Al-Wugayan, Adel A. (2020) Customer Relationships in Banking: Does relationship strength influence relationship quality and outcomes?, Studies in Business and Economics, 23(1), 61-97. https://doi.org/10.29117/sbe.2020.0121

- Ali, A., & Daly, K. J. (2010). Modelling credit risk : a comparison of Australia and the USA. Journal Of International Finance And Economics, 10(1), 123-131. http://handle.uws.edu.au:8081/1959.7/552730

- Ali, A.,Sabir, H. M., Sajid, M &Taqi, M (2014), “Do non performing loan affect bank performance? evidence from listed banks at Karachi stock exchange (KSE) of Pakistan” The International Journal of Interdisciplinary Social Sciences: Annual Review 4(1):363-377

- Al-Khouri, R. (2011). Assessing the risk and performance of the GCC banking sector, International Journal of Finance and Economics, 63(5), 72-84

- Amoako, G., Arthur, E., Bandoh, C., & Katah, R, (2012). The impact of effective customer relationship management (CRM) on repurchase: A case study of (GOLDEN TULIP) hotel (ACCRA-GHANA). African Journal of Marketing Management, 4(1), 17-29. DOI: 10.5897/AJMM11.104

- Beck, Thorsten, Asli Demirgüç-Kunt, and Levine, Ross (2003) “Law, endowments, and finance”, Journal of Financial Economics, 70(2), 137-181 https://doi.org/10.1016/S0304-405X(03)00144-2

- Berger, Allen N., and Robert DeYoung. (1997). Problem Loans and Cost Efficiency in Commercial Banks. Journal of Banking & Finance 21(6): 849–70. https://doi.org/10.1016/S0378-4266(97)00003-4

- Bhat, Gauri and Desai, Hemang(2020) Bank Capital and Loan MonitoringThe Accounting Review 95(3), 85-114, https://doi.org/10.2308/accr-52587

- Brealey, R. and Myers, S. (2005). Principles of corporate finance (8th edition), London: McGraw-Hill.

- Cerqueiro, G., Ongena, S. & Roszbach, Kasper (2016) Collateralization, Bank Loan Rates, and Monitoring, Journal of Finance, 71(3), 1295-1322 https://doi.org/10.1111/jofi.12214

- Chen, K., & Pan, C. (2012). An empirical study of credit risk efficiency of banking industry in Taiwan. Web Journal of Chinese Management Review, 15(1), 1-16.

- Cipovová, Eva & Jílková, Petra (2018) “Loan Product Policy and Rentability Based on Interest Rates in Czech Republic” European Research Studies Journal, 21(2), 575-585, DOI: 10.35808/ersj/1024

- Dhman Z. A. (2011). The Effect of Customer Relationship Management (CRM) Concept Adoption on Customer Satisfaction–Customers Perspective: The Case of Coastal Municipalities Water Utility CMWU-Rafah Branch. (Master Thesis- Unpublished), Islamic University-Gaza Strip

- Disemadi, Hari Sutra (2019) “Risk management in the provision of people’s business credit as implementation of prudential principles”, Diponegoro Law Review , 4(2)194-208. https://ejournal.undip.ac.id/index.php/dlr/article/view/24904

- Duncan, E. & Elliot, G (2004) “Efficiency, Customer service and financial performance among Australian financial institutions”International Journal of Bank Marketing 22(5):319-342. DOI:10.1108/02652320410549647

- Epure, M. and Lafuente, I. (2012). Monitoring Bank Performance in the Presence of Risk. Barcelona GSE Working Paper Series No.61.https://upcommons.upcedu/bitstream/handle/2117/27455/Epure_&_Lafuente_GSE%20WP613.pdf

- Frattaroli, Marc & Herpfer, Christoph (2023) “Information Intermediaries: How Commercial Bankers Facilitate Strategic Alliances” Journal Of Financial And Quantitative Analysis, 58(2), 543–573. doi:10.1017/S0022109022000485

- Gabriel, O., Victor, I. E., & Innocent, I. O. (2019). Effect of non-performing loans on the financial performance of commercial banks in Nigeria. American International Journal of Business and Management Studies, 1(2), 1-9 https://doi.org/10.46545/aijbms.v1i2.115

- Ghandi, R. (2014). Banks debt recovery and regulations, India: Bank for International Settlements. https://www.bis.org/review/r150109f.html

- Hamisu S.K (2011). Credit risk and the performance of Nigerian banks. Department of accounting Faculty of Administration Ahmadu Bello University, Zaria – Nigeria

- Innes, Mitchell (1914) “The Credit Theory of Money”The Banking Law Journal, 31, 151-168. https://www.academia.edu/2475676/Credit_and_State_Theories_of_Money_The_Contributions_of_A_Mitchell_Innes

- Kaczmarczyk, Katarzyna (2019) Methods for calculating loan profitability for a bank Central European Review of Economics & Finance 29(1), 5-22 https://doi.org/10.24136/ceref.2019.001

- Kashiv, Rajeev (2021) "NPA And Recovery Performance In Banks: An Exploratory Research In A Rural Co-Operative Bank" International Journal of Creative Research Thoughts (IJCRT) 9(11), 21-26. https://ijcrt.org/papers/IJCRT2111117.pdf

- Kavita, P., Wamitu, S. & Nzomoi, J (2022) Relationship between Bank Customer Retention Strategies and Customer Satisfaction in Commercial Banks in Machakos Town. European journal of business and strategic management 7(2), 23 - 38, https://www.iprjb.org/journals/index.php/EJBSM/article/view/1640

- Kargi, H.S. (2011). Credit risk and the performance of Nigerian banks, AhmaduBello University, Zaria

- Khanum, R &Sumathi, K (2021)“Recovery of Non-performing assets- A challenge for Indian Financial Institutions”Anusandhan - NDIM’s Journal of Business and Management Research3(1), 51-59, https://doi.org/10.56411/anusandhan.2021.v3i1.51-59

- Kithinji, A.M. (2010). Credit risk management and profitability of commercial banks in Kenya, School of Business, University of Nairobi, Nairobi

- Krishnamoorthy, V., & Srinivasan, R. (2013). The Impact of Customer Relationship Management on Loyalty in Indian Banking Sector–An Empirical Study. International Monthly Refereed Journal of Research In Management & Technology, 11(June), 150-161.

- Manoj Kumar Sahoo and Dr. Muralidhar Majhi (2020), “The Recovery Management System of NPAs-A Case study of Commercial Banks in India”, Parishodh Journal,9(3).5065-5076 DOI:09.0014.PARISHODH.2020.V9I3.0086781.57506

- Meghana, P. S,& Supriya, R. (2020) “Role of Commercial Banks in Achieving Financial Inclusion – A Comparative Study of Canara Bank and Corporation Bank”, Studies in Indian Place Names 40(25), 1-11 https://ssrn.com/abstract=3838593

- Migwi, J. M (2013) Credit Monitoring and recovery strategies adopted by Commercial Banks in Kenya, Masters degree thesis submitted to Business Administration School Of Business, University Of Nairobi

- Muiru, M. S., Oluoch, W. O &Ajang, J. J (2018), “Effect of loan portfolio management on the profitability of deposit taking microfinance institutions in Nairobi, Kenya”, International Journal of Economics, Commerce and Management 6(2).

- Nkusu, Mwanza. 2011. “Nonperforming Loans and Macrofinancial Vulnerabilities in Advanced Economies.” International Monetry Fund Working Paper 11/161.

- Offiong, A. I & Egbuka, N (2017) The Efficency of Loan Recovery Rate in Deposit Money Banks in Nigeria, Journal of Finance and Bank Management 5(2), 40-49. DOI:10.15640/jfbm.v5n2a4

- Omitogun, O., Olanrewaju, D & Alalade, Y. S. A (2016) Loans Default and Return on Assets (ROA) In the Nigerian Banking System, International Journal of Economics and Financial Research 2(4) 65-73, http://arpgweb.com/?ic=journal&journal=5&info=aims

- Ozurumba, B A.(2016) Impact of Non-Performing Loans on the Performance of Selected Commercial Banks in Nigeria, Research Journal of Finance and Accounting 7(16), 95-109

- Robert D. & Gary W. (1994): “Banking Industry Consolidation: efficiency Issues”, working paper No. 110 presented at the financial system in the decade ahead: A Conference of the Jerome Levy Economics Institute April 14-16, 1994.

- Saka, R. O., Elegunde, A. F.&Lawal, A.Y. (2014)“Effects of Customer Relationship Marketing on Bank Performance in Nigeria: An Empirical Approach” Indian Journal of Commerce and Management Studies, 5(3), 89-93http://scholarshub.net/index.php/ijcms/article/view/195/189

- Salas, Vincente, and Jesus Saurina. 2002. “Credit Risk in Two Institutional Regimes: Spanish Commercial and Savings Banks.” Journal of Financial Services Research, 22(3): 203-224.

- Shavazi, E. T., Moshabaki, A., Hoseini, S. H., Naiej, A. K. (2013). Customer Relationship Management and Organizational Performance: A Conceptual Framework Based On the Balanced Scorecard (Study of Iranian Banks). Journal of Business and Management (IOSR-JBM) 10(6), 18-26. https://doi.org/10.9790/487X-1061826

- Siraki, Queen & Yona, Lucky (2021) "Factors Influencing the Recovery of Non-Performing Loans in Commercial Banks: The Case of Exim Bank, European Journal of Business and Management 13(14), 29-43, https:// 10.7176/EJBM/13-14-05

- Stephen, Murey Yego & Joseph ,Gichure (2020), “Effect of debt recovery policy on performance of commercial banks in Kitale Town, Kenya”, International Journal of Recent Research in Commerce Economics and Management (IJRRCEM), 7(4), 94-115

- Sudin Bag and Sajijul Islam (2017), “Non-Performing Assets A Biggest Challenge in Banking Sector - Comparative Study Between Indian and Bangladesh Banking Sector”, ICTACT Journal on management studies, 3(4).620-624 https//10.21917/ijms.2017.0084

- Yeruva Priyanka and Ch. Rajesh Kumar (2019), “Non-performing Assets of Commercial Banks and its Recovery in India”, Complexity International Journal, 23,(2). 1320-0682

This work is licensed under a Creative Commons Attribution 4.0 International License.